Right now, publicly traded companies across the country are spending significant time and resources preparing to report the ratio of their CEOs’ pay to the pay of their median employees for the first time. That’s because the Securities and Exchange Commission (SEC) new pay ratio disclosure rule just took effect for the 2018 proxy season, following enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010.

By the SEC’s own calculations, the rule will cost employers $1.3 billion in 2018. But exactly what will it achieve? Proponents of the rule say shareholders will have a new metric to measure CEO salaries. Unfortunately, the rule is fundamentally flawed and particularly ill-suited for making fair comparisons between companies in different industries with differing business models. As a result, large sums of money and considerable time and effort will be spent on producing a misleading metric that generates little value for shareholders.

Retail wages compare quite favorably against other industries when part-time and temporary workers are removed from the equation.

The core of the problem rests with how the ratio is calculated: It is heavily biased against businesses that rely on seasonal and part-time workers. The rule states that for the day of the year on which the median salary is computed, every worker on that date — including part-time, temporary and seasonal workers — must be included in the median. It also states that while permanent employees’ salaries can be annualized, the same cannot be done for part-time, temporary and seasonal employees. The partial salaries of non-permanent employees will pepper the bottom end of the salary distribution and pull the median down dramatically for companies that disproportionately rely on a flexible workforce.

Retail wages compare quite favorably against other industries when part-time and temporary workers are removed from the equation. According to data from Mercer, the average wage for full-time retail employees is $28 an hour,* equating to an annual salary in excess of $50,000. An apples-to-apples comparison of full-time workers would provide a much more meaningful metric; as it’s written, the rule doesn’t reflect the realities or needs of the nation’s diverse workforce.

There’s no better example of this than the retail industry, where 30 percent of workers are part-time. Retailers run their stores to make it convenient for people to shop. If a consumer wants something in the middle of the evening, shops primarily on weekends or shops more during the holiday season, retailers respond to those needs. To do this, they scale up their workforces at peak times and often have a round-the-clock presence.

Companies that provide flexible work opportunities will be under attack based on unfair, apples-to-oranges comparisons.

Retail provides jobs for millions of Americans who are looking for flexible work opportunities. That includes students trying to afford college tuition, people caring for a child or aging family member, senior citizens looking to supplement retirement income and disabled workers who can’t work full schedules. Retail jobs are also where America’s teenagers gain their first experience in the workforce — in fact, retail employs a quarter of the nation’s working teenagers.

An estimated 75 percent of part-time workers choose this schedule. It’s hard to imagine an economy without these types of jobs, or where many other industries would be without the job training their employees received in retail.

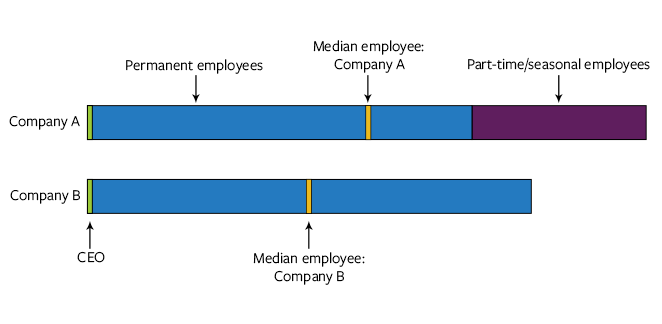

Yet under the SEC pay ratio rule, companies that provide these opportunities will be under attack based on unfair, apples-to-oranges comparisons. Consider an example of two companies with exactly 100 permanent employees and the same pay scales. The first employee makes $1 a year and the 100th employee makes $100. Everyone else makes a salary in increments of a dollar: Employee two makes $2, employee three makes $3 and so on.

Now consider that both companies are doing well and need more employees. Company A’s demand fluctuates and requires staff that can fill in hours during busy periods, so it hires 20 part-time workers and 25 seasonal workers to cope with the growing demand. These part-time and seasonal employees work enough hours during the year to equate to 15 full-time employees. Company B, with a completely different business model, has more constant demand and hires 15 full-time workers to cope with a similar increase in demand. To make the math easier to follow, assume all 15 new employees’ wages fall at the bottom end of the salary spectrum, as with Company A.

NRF advocates for a fair pay ratio rule. Read about why it matters to retailers.

Assuming the CEO’s salary is the $100 at the top end of the distribution, the CEO-to-worker pay ratio for Company A would be 3.6x versus only 2.3x for Company B — a tremendous difference in the ratio for two companies with identical CEO salaries and similar hours worked by their employees.

It simply does not make sense to include part-time and seasonal workers in calculating a CEO-to-worker pay ratio, especially if companies are not allowed to annualize their salaries. Comparing a full-time CEO’s salary to a workforce that includes employees working a few hours a week or a few weeks per year does not make for an accurate metric, given the disparity in the labor force across industries. At the very least, companies should be allowed to annualize the salaries of part-time workers and those who have only been employed for a short period of time. It might still result in a distorted ratio as calculated above, but it would be nowhere near as skewed and would provide a fairer comparison.

This rule penalizes companies for catering to the needs of consumers. It shames retailers for providing flexible job opportunities and entry-level work for America’s young people. And it demoralizes those getting started in their careers and climbing the economic ladder. What it won’t do is provide a valid measure of CEO-to-worker pay disparity, which means companies will spend significant time and resources providing the public with a metric that fails to provide any information of value.

* This average is calculated on an organization-weighted basis. Source: Mercer US Retail Compensation & Benefits Survey